Global High Purity Indium Metal Market to Reach USD 815.7 Million by 2034 as Displays, Semiconductors, and Solar Technologies Drive Demand

High Purity Indium Metal is a refined specialty metal known for its silvery-white appearance, exceptional ductility, low melting point, and strong electrical conductivity. Unlike many conventional industrial metals, indium is valued not for bulk structural use but for its ability to enable advanced electronic, optical, and energy-related technologies.

The material is commonly refined into ultra-high purity grades such as 4N (99.99%), 5N (99.999%), and 6N (99.9999%). These purity levels are essential for applications where even trace impurities can affect conductivity, transparency, semiconductor performance, or device reliability. High purity indium is especially important in Indium Tin Oxide (ITO) coatings, compound semiconductors, solder alloys, thermal interface materials, photovoltaics, sensors, and next-generation electronic devices.

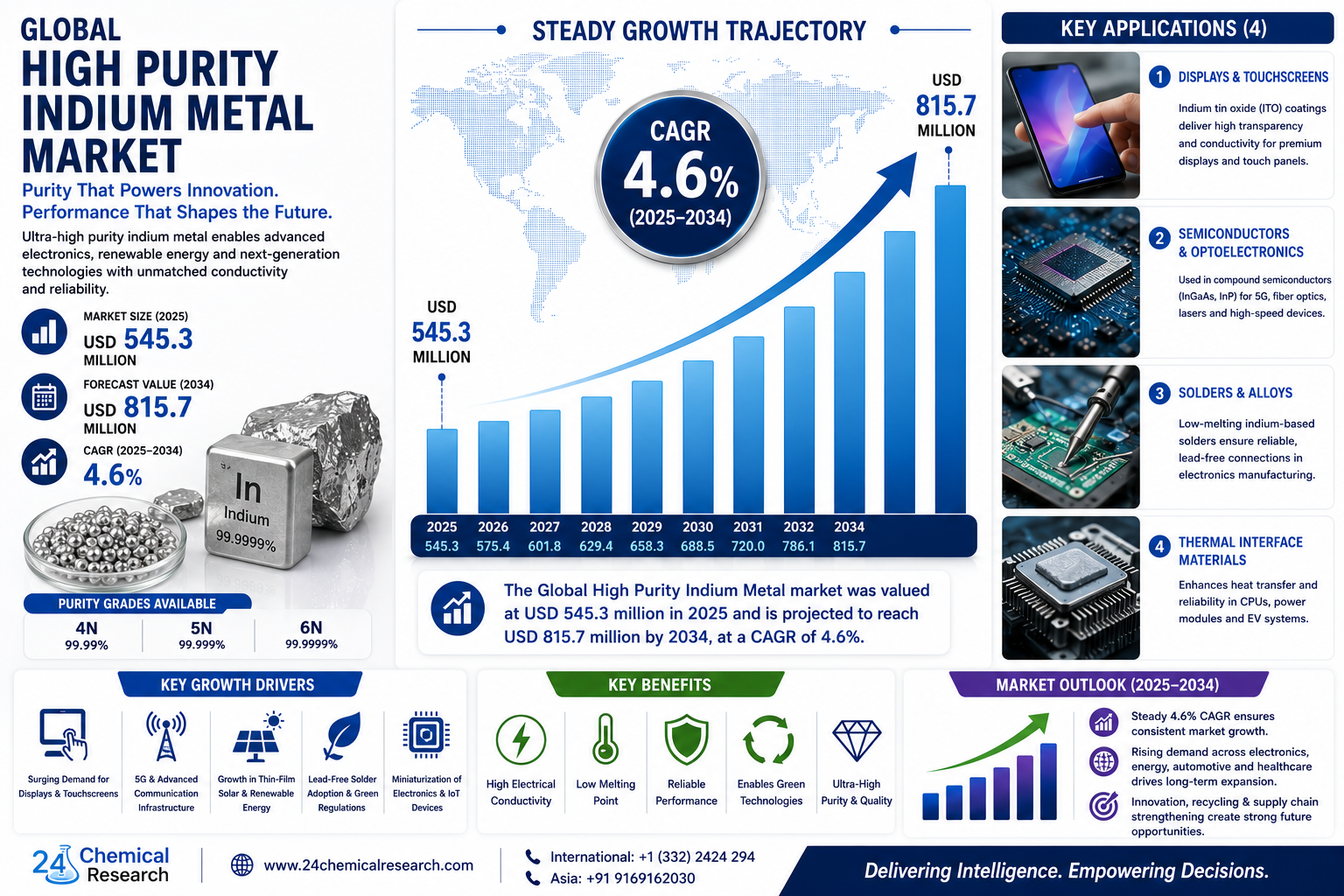

The Global High Purity Indium Metal market was valued at USD 545.3 million in 2025 and is projected to reach USD 815.7 million by 2034, exhibiting a steady CAGR of 4.6% during the forecast period. Market growth is being supported by rising demand from display technologies, consumer electronics, 5G infrastructure, compound semiconductors, lead-free soldering, electric vehicles, renewable energy systems, and high-performance thermal management applications.

Get Full Report Here:

https://www.24chemicalresearch.com/reports/307151/high-purity-indium-metal-market

Market Dynamics:

The High Purity Indium Metal market is shaped by a complex interplay of strong technology-led demand, supply chain vulnerability, byproduct dependency, recycling limitations, and emerging opportunities in next-generation electronics and sustainable technologies. As global industries continue to invest in digital infrastructure, energy-efficient devices, and renewable power systems, high purity indium is becoming increasingly important across the electronics and advanced materials value chain.

Key Market Highlights

● Global High Purity Indium Metal market was valued at USD 545.3 million in 2025 and is projected to reach USD 815.7 million by 2034.

● The market is expected to grow at a steady CAGR of 4.6% during the forecast period.

● 4N purity indium currently dominates the market due to its cost-effectiveness and broad use in ITO coatings and soldering applications.

● 5N and 6N purity grades are gaining momentum in compound semiconductors, photonics, optoelectronics, and advanced electronics.

● ITO remains the largest application segment, supported by demand from touchscreens, LCDs, OLED displays, and transparent conductive films.

● Asia-Pacific holds more than 70% of the global market, driven by electronics manufacturing strength in China, Japan, and South Korea.

● Recycling, IoT applications, smart windows, photovoltaics, and vertical integration offer major future growth opportunities.

Powerful Market Drivers Propelling Expansion

-

Expansion of Display Technologies and Consumer Electronics:

The rapid expansion of display technologies is the primary growth driver for the High Purity Indium Metal market. Indium is widely used in Indium Tin Oxide, commonly known as ITO, which serves as a transparent conductive coating in touchscreens, LCDs, OLED panels, flat-panel displays, and photovoltaic devices.

ITO coatings are valuable because they combine optical transparency with electrical conductivity. This makes them essential for devices that must allow light transmission while also supporting touch response, signal transfer, or electronic control. Smartphones, tablets, laptops, televisions, automotive displays, smart watches, and industrial touch panels all depend on transparent conductive materials.

The global display market, valued at over $150 billion, continues to expand as consumers and industries demand higher-resolution screens, thinner devices, better touch sensitivity, and improved energy efficiency. This supports consistent demand for high purity indium used in ITO production.

Flexible and foldable displays are also creating new requirements for ultra-high purity indium grades. These advanced display formats require materials that can maintain conductivity and performance under bending, repeated use, and compact device design. As consumer electronics continue to evolve, high purity indium remains a cornerstone material for screen innovation and transparent conductive technologies.

-

Growth in Compound Semiconductors and Photovoltaics:

High purity indium is increasingly important in compound semiconductor materials such as indium gallium arsenide (InGaAs) and indium phosphide (InP). These materials are used in 5G infrastructure, fiber-optic communication systems, photodetectors, laser diodes, infrared sensors, high-speed electronics, and advanced optoelectronic devices.

Compound semiconductors offer performance advantages over traditional silicon in specific high-frequency, high-speed, and optoelectronic applications. Indium-based semiconductor compounds help enable faster data transmission, better signal processing, and improved detection capabilities. This makes them important for telecommunications, defense electronics, aerospace, data centers, and advanced sensing systems.

The compound semiconductor market is anticipated to exceed $44 billion, and indium remains a critical material for several of its high-value applications. As 5G deployment, cloud infrastructure, AI hardware, fiber optics, and photonics continue expanding, demand for high-purity indium inputs is expected to strengthen.

Photovoltaics also contribute to market demand. Thin-film solar technologies and selected advanced photovoltaic materials incorporate indium due to its electronic and conductive properties. As renewable energy investments rise globally, indium’s role in energy-related applications continues to gain importance.

-

Advancements in Solder and Thermal Interface Materials:

Indium-based solders and thermal interface materials are widely used in electronics manufacturing because of their low melting point, strong wetting properties, and reliability in sensitive applications. These materials are especially useful where components cannot tolerate high processing temperatures.

The global shift toward lead-free soldering has accelerated demand for alternative solder alloys. Environmental regulations and electronics industry standards are encouraging manufacturers to reduce or eliminate lead from electronic assemblies. Indium-containing solders help meet these requirements while providing strong performance in specialized applications.

In high-performance computing, electric vehicles, power electronics, aerospace systems, and advanced semiconductor packaging, heat dissipation is a major design concern. Indium-based thermal interface materials help transfer heat away from sensitive components, improving reliability and extending device lifespan.

As electronic systems become more compact and powerful, thermal management becomes increasingly important. This supports sustained demand for high purity indium in solders, bonding materials, interface layers, and advanced packaging applications.

Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/307151/high-purity-indium-metal-market

Significant Market Restraints Challenging Adoption

Despite its strong role in advanced technologies, the High Purity Indium Metal market faces several hurdles that must be addressed to support broader and more stable adoption.

-

Supply Chain Vulnerabilities and Price Volatility:

One of the most important restraints in the High Purity Indium Metal market is supply vulnerability. Indium is primarily recovered as a byproduct of zinc mining and refining. This means supply is tied to zinc production levels rather than direct indium demand.

When zinc production declines or refining economics shift, indium availability can tighten even if demand from electronics or semiconductors remains strong. This byproduct dependency creates structural supply uncertainty.

Price volatility is another major challenge. Annual price swings of 20-30% are not uncommon due to supply-demand imbalances, speculative activity, recycling limitations, and disruptions in zinc production. Such volatility complicates procurement planning for display manufacturers, semiconductor producers, and electronics companies.

Geopolitical concentration adds further risk. China accounts for over 60% of global primary indium production, making global supply vulnerable to trade policies, export restrictions, domestic industrial priorities, and regional regulatory changes. For manufacturers outside Asia, this concentration increases the need for diversified sourcing, recycling, and long-term supply agreements.

-

High Production Costs and Technical Barriers:

Producing ultra-high purity indium, especially 6N (99.9999%) grade, requires complex refining processes such as electrolytic refining, zone refining, and vacuum distillation. These methods need specialized equipment, controlled environments, strict impurity monitoring, and skilled technical expertise.

Production costs for ultra-high purity grades can be 20-40% higher than those for standard metals. This creates cost barriers, especially in applications where end-users are price-sensitive or where lower-purity materials may be technically acceptable.

Maintaining consistent quality at commercial scale is also challenging. Semiconductor, optoelectronic, and advanced display applications require extremely tight impurity control. Even small variations in purity can affect conductivity, transparency, device yield, or long-term reliability.

These technical barriers limit the number of suppliers capable of producing high-purity grades consistently. They also increase qualification timelines for customers, making supplier relationships and quality assurance especially important.

Critical Market Challenges Requiring Innovation

The transition from laboratory-scale purification to industrial-scale production presents significant challenges for the High Purity Indium Metal market.

Scaling purification processes to produce high volumes of 6N purity indium remains difficult. In some cases, yields may fall below 70% because of strict quality requirements and the difficulty of removing trace impurities. Lower yields increase production costs and limit supply availability for high-end applications.

Recycling is another major challenge. Current indium recovery rates remain below 30%, despite the material’s use in high-volume electronic products such as displays and touchscreens. Much of the indium used in ITO coatings is thinly dispersed across glass or electronic components, making recovery technically complex and economically challenging.

Limited recycling infrastructure increases reliance on primary production and exposes the market to zinc mining dynamics. Improving recovery from end-of-life electronics, manufacturing scrap, sputtering targets, and display panels will be essential for long-term supply stability.

The market also faces logistical and regulatory complexity. High-purity metals require careful handling, storage, packaging, and transport to avoid contamination. Inconsistent regional regulations for recycling and material handling create additional complexity for global suppliers.

Specialized producers often need to invest 15-20% of revenue into research and development to improve purification yields, recycling technologies, and product quality. This creates barriers for new entrants and reinforces the position of established companies with technical expertise and capital strength.

Vast Market Opportunities on the Horizon

-

Next-Generation Electronics and IoT Applications:

The rise of next-generation electronics and Internet of Things applications presents a strong opportunity for the High Purity Indium Metal market. IoT devices, wearable electronics, smart sensors, flexible circuits, connected appliances, and advanced communication systems require materials that combine conductivity, flexibility, reliability, and miniaturized performance.

Indium-based materials are well suited for these applications because they support transparent conductive coatings, flexible electronics, low-temperature soldering, and compact electronic assembly. As devices become smaller and more connected, demand for reliable conductive and thermal materials is expected to rise.

Wearable devices and smart sensors are particularly relevant because they often require thin, lightweight, and flexible electronic components. Indium-based compounds and coatings can support the development of flexible displays, touch interfaces, biosensors, and energy-efficient circuits.

As IoT adoption expands across healthcare, industrial automation, smart homes, logistics, automotive systems, and consumer electronics, high purity indium may find broader use in sensors, transparent electrodes, microelectronic components, and advanced interconnect materials.

-

Sustainable Technologies and Circular Economy Initiatives:

Sustainability and circular economy initiatives represent one of the most important long-term opportunities for the High Purity Indium Metal market. Because indium supply is constrained by byproduct recovery, recycling can play a critical role in improving supply stability and reducing dependency on primary sources.

End-of-life electronics, display panels, ITO sputtering targets, semiconductor scrap, and manufacturing residues all represent potential sources of secondary indium. Advances in recycling technologies could potentially increase recovery rates to 50% or higher, creating a more resilient supply chain.

Circular economy models are especially important for electronics and display manufacturers seeking to reduce material waste and improve sustainability performance. Closed-loop recovery of indium from production scrap and used electronics can help stabilize supply while reducing environmental impact.

Indium also supports sustainable technologies such as smart windows, advanced photovoltaics, energy-efficient electronics, and thermal management systems. These applications align with global goals for energy efficiency, renewable energy deployment, and resource conservation.

-

Strategic Collaborations and Vertical Integration:

Strategic collaborations are becoming increasingly important in the High Purity Indium Metal market. Producers, refiners, electronics manufacturers, semiconductor companies, and renewable energy firms are forming partnerships to secure supply and develop application-specific materials.

These collaborations help align indium production with emerging technology needs. For example, display manufacturers may require specific ITO-grade indium, while semiconductor companies may need 5N or 6N material with strict impurity limits. End-user collaboration helps producers tailor products more effectively.

Vertical integration is also becoming a key strategy. Companies that control or coordinate zinc refining, indium recovery, purification, recycling, and downstream product supply can reduce risk and improve supply reliability.

Long-term supply agreements are particularly valuable in markets where material qualification is expensive and time-consuming. Once high purity indium is approved for semiconductor, display, or advanced electronics use, customers often prefer stable suppliers with consistent quality and reliable delivery.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into:

● 4N (99.99%)

● 5N (99.999%)

● 6N (99.9999%)

4N purity currently dominates the High Purity Indium Metal market due to its cost-effectiveness and suitability for a wide range of applications. It is widely used in ITO production, general soldering, alloys, and electronic materials where ultra-high purity is not always required.

5N purity indium is gaining demand in applications that require stronger impurity control, including advanced electronics, semiconductor materials, optoelectronics, and high-performance sputtering targets. It offers improved reliability for more demanding applications.

6N purity indium represents a smaller but rapidly growing high-value segment. It is used in advanced semiconductors, photonics, compound semiconductor materials, research-grade applications, and highly sensitive optoelectronic devices. Because of its technical production complexity, 6N indium commands premium pricing.

As semiconductor, photonics, and advanced display technologies continue to mature, demand for 5N and 6N grades is expected to grow faster than standard grades.

By Application:

Application segments include:

● ITO (Indium Tin Oxide)

● Semiconductors

● Solders and Alloys

● Others

The ITO segment holds the largest market share. ITO coatings are essential in touchscreens, LCDs, OLED displays, flat-panel displays, smart windows, and transparent conductive films. The continuous growth of display technologies and touchscreen devices supports strong demand from this segment.

The Semiconductor segment is expected to show the highest growth. Indium-based compound semiconductors such as InGaAs and InP are used in 5G infrastructure, photodetectors, fiber-optic communication, laser diodes, infrared sensors, and high-speed electronics. These applications require increasingly pure indium inputs.

Solders and Alloys remain an important application area. Indium-based solders are used in low-temperature bonding, lead-free soldering, thermal interface materials, and high-reliability electronic assemblies. This segment benefits from environmental regulations and rising demand for advanced electronics packaging.

Other applications include photovoltaics, smart windows, specialty coatings, research materials, thermal management systems, and advanced energy technologies.

By End-User Industry:

The end-user landscape spans:

● Electronics

● Automotive

● Energy

● Healthcare

The Electronics industry remains the dominant consumer of high purity indium. Displays, semiconductors, soldering materials, optoelectronics, sensors, and electronic packaging account for a major share of demand.

The Automotive sector is gaining importance as vehicles become more digital, electrified, and connected. Indium is used in displays, sensors, advanced driver assistance systems, thermal interface materials, and power electronics. Electric vehicles also create additional demand for reliable thermal management and low-temperature bonding materials.

The Energy sector is emerging as a key growth area. Indium is used in photovoltaics, smart windows, energy-efficient coatings, and thermal management systems. As renewable energy and energy-saving technologies expand, indium’s role in sustainable applications may increase.

Healthcare applications include medical sensors, imaging technologies, optoelectronic devices, wearable health monitors, and diagnostic equipment. Although smaller in volume, these applications often require high reliability and specialized materials.

Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/307151/high-purity-indium-metal-market

Frequently Asked Questions

What is High Purity Indium Metal used for?

High Purity Indium Metal is used in Indium Tin Oxide coatings, touchscreens, LCDs, OLED displays, compound semiconductors, solder alloys, thermal interface materials, photovoltaics, smart windows, sensors, and advanced electronics. Its conductivity, ductility, low melting point, and ability to form transparent conductive oxides make it valuable in high-tech applications.

What is driving the High Purity Indium Metal market?

The High Purity Indium Metal market is driven by growth in display technologies, consumer electronics, 5G infrastructure, compound semiconductors, photovoltaic technologies, lead-free soldering, electric vehicles, and advanced thermal management. Rising demand for transparent conductive materials and high-performance electronic components is supporting market expansion.

Which purity grade dominates the High Purity Indium Metal market?

4N purity indium currently dominates the market because it offers a practical balance of performance and cost. It is widely used in ITO production, general soldering, alloys, and electronic materials. However, 5N and 6N grades are growing quickly in semiconductors, photonics, and optoelectronic applications.

Which application segment leads the market?

ITO, or Indium Tin Oxide, is the largest application segment. ITO coatings are widely used in touchscreens, LCDs, OLED displays, transparent conductive films, and smart windows. Demand is supported by continued growth in consumer electronics, display technologies, and digital devices.

Why is indium supply vulnerable?

Indium supply is vulnerable because it is mainly recovered as a byproduct of zinc mining and refining. Its availability depends on zinc production rather than direct indium demand. China’s dominance in primary indium production also creates geopolitical and trade-related supply risks.

Competitive Landscape:

The global High Purity Indium Metal market is moderately consolidated, characterized by robust competition, technical specialization, and a strong focus on purification technology. Leading companies compete through production capacity, purity control, R&D strength, recycling capabilities, customer relationships, and global distribution networks.

The top three companies—Korea Zinc (South Korea), Dowa Holdings (Japan), and Umicore (Belgium)—collectively account for approximately 50% of the market share as of 2025. Their leadership is supported by strong production capabilities, advanced refining technologies, recycling expertise, and established relationships with electronics, semiconductor, and energy customers.

List of Key High Purity Indium Metal Companies Profiled:

● Korea Zinc (South Korea)

● Dowa Holdings (Japan)

● Umicore (Belgium)

● Asahi Holdings (Japan)

● Teck Resources (Canada)

● Nyrstar (Switzerland)

● YoungPoong (South Korea)

● PPM Pure Metals GmbH (Germany)

● China Germanium (China)

● Zhuzhou Smelter Group (China)

● GreenNovo (China)

The competitive strategy is heavily centered on research and development. Companies are investing in technologies that improve purity levels, increase refining yields, reduce production costs, and strengthen recycling efficiency.

Strategic partnerships with electronics, semiconductor, display, and energy companies are also becoming more common. These collaborations help producers co-develop tailored indium grades, secure long-term demand, and support application-specific innovation.

As demand for 5N and 6N indium grows, suppliers that can consistently deliver ultra-high purity material with strong quality documentation are expected to gain competitive advantage.

Regional Analysis: A Global Footprint with Distinct Leaders

● Asia-Pacific:

Asia-Pacific is the dominant region in the High Purity Indium Metal market, holding over 70% of the global market. This leadership is driven by strong electronics manufacturing, zinc mining and refining activity, semiconductor production, and display panel manufacturing in China, Japan, and South Korea.

China is both the largest producer and consumer of high purity indium. Its leadership is supported by primary indium production, government-backed high-tech industry development, display manufacturing, solar technology, and electronics production.

Japan plays a major role in high-purity indium processing, advanced electronics, semiconductor materials, and precision manufacturing. Japanese companies are known for quality control and technical expertise in high-performance materials.

South Korea contributes strong demand through its display, semiconductor, electronics, and battery industries. The country’s advanced manufacturing base supports demand for ITO coatings, compound semiconductors, and high-purity electronic materials.

Asia-Pacific’s integrated supply chain gives the region a strong advantage, but it also makes global markets dependent on Asian production and policy conditions.

● North America and Europe:

North America and Europe together account for approximately 25% of the High Purity Indium Metal market. Both regions are important demand centers for advanced semiconductors, renewable energy technologies, electronics, aerospace, and high-value manufacturing.

North America benefits from strong semiconductor R&D, renewable energy investment, defense electronics, and advanced materials development. The region is also increasingly focused on domestic supply chain security for critical materials, including indium.

Europe’s market is shaped by stringent quality standards, sustainable technology development, recycling initiatives, and demand from electronics, automotive, renewable energy, and specialty manufacturing sectors. The region is actively investing in circular economy solutions to reduce dependence on imported critical materials.

Both North America and Europe are working to improve recycling infrastructure and domestic recovery capabilities. These efforts are important because primary indium production remains concentrated in Asia, particularly China.

● Rest of the World:

Other regions, including South America and the Middle East & Africa, currently represent smaller shares of the High Purity Indium Metal market but offer future growth potential.

South America may gain relevance through mining, base metal refining, industrialization, and future opportunities in critical mineral recovery. As regional manufacturing and renewable energy projects expand, demand for specialty metals may increase.

The Middle East & Africa represent emerging markets where technological adoption, electronics consumption, solar energy investment, and industrial development could create gradual demand growth. Solar energy projects in high-irradiance regions may support future use of indium-containing photovoltaic technologies.

As global supply chains diversify, these regions may become more important in long-term sourcing, processing, and demand development.

Get Full Report Here:

https://www.24chemicalresearch.com/reports/307151/high-purity-indium-metal-market

Download FREE Sample Report:

https://www.24chemicalresearch.com/download-sample/307151/high-purity-indium-metal-market

Need More In-Depth Market Intelligence?

The complete report provides detailed insights into:

✔ Regional demand forecasts

✔ Production capacity analysis

✔ Pricing trends

✔ Competitive landscape

✔ Supply chain developments

✔ Emerging opportunities

✔ Purity-grade demand analysis

✔ Application-wise growth outlook

✔ Recycling and circular economy trends

Access the Full Report:

https://www.24chemicalresearch.com/reports/307151/high-purity-indium-metal-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a trusted provider of chemical market intelligence, serving clients including over 30 Fortune 500 companies. The company provides data-driven insights through rigorous research methodologies, helping businesses understand government policy, emerging technologies, competitive landscapes, production capacity, pricing movements, and supply chain developments.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030