Organophosphine Ligand Market Surges on Catalysis & Pharmaceutical Manufacturing Demand

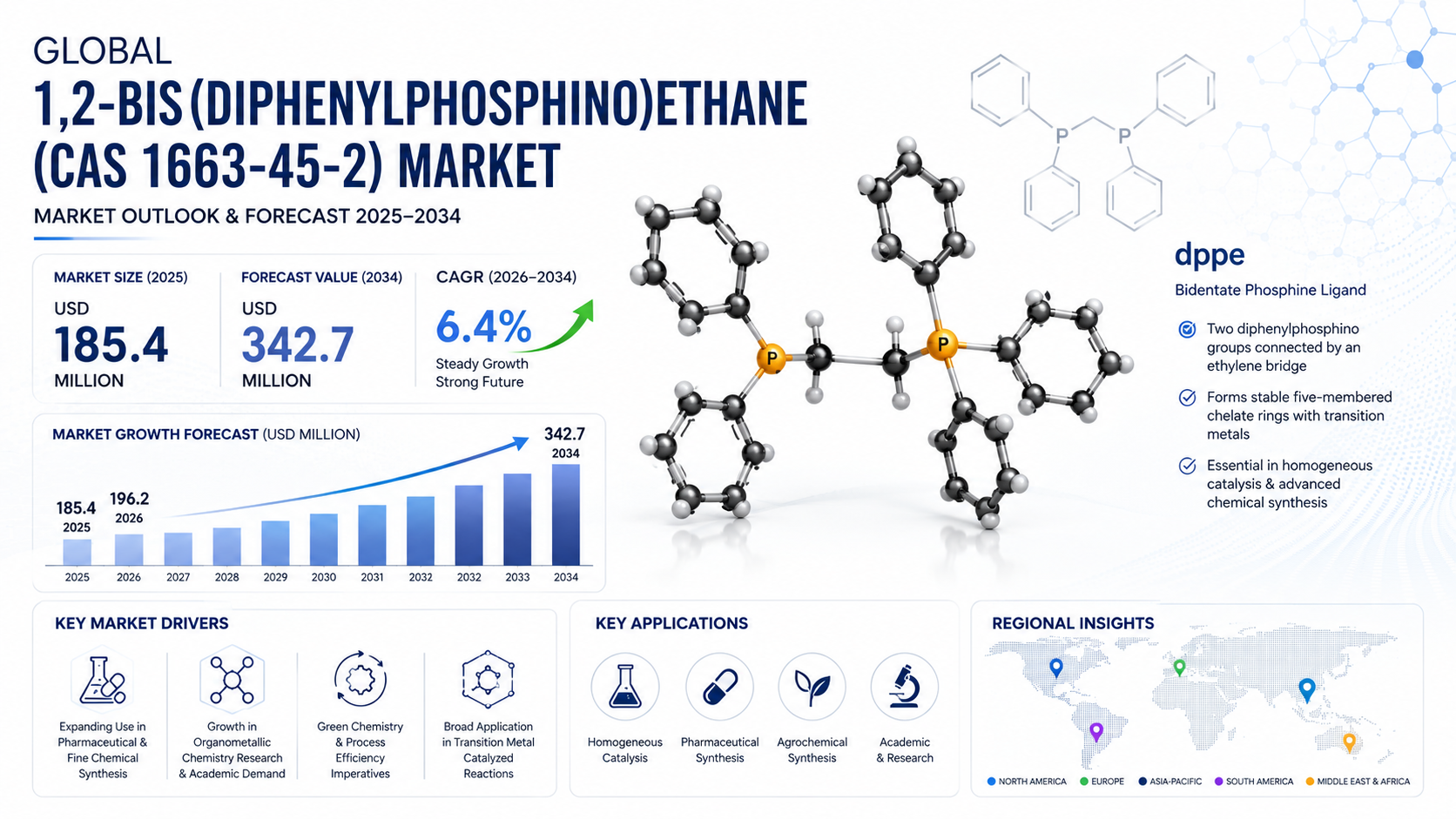

Global 1,2-Bis(diphenylphosphino)ethane (CAS 1663-45-2) market size was valued at USD 185.4 million in 2025. The market is projected to grow from USD 196.2 million in 2026 to USD 342.7 million by 2034, exhibiting a CAGR of 6.4% during the forecast period.

1,2-Bis(diphenylphosphino)ethane, widely known in the scientific community as dppe or DPPE, is a bidentate organophosphorus ligand that has carved out an indispensable role in both academic research and industrial chemistry over the past several decades. The compound features two diphenylphosphino groups connected by a two-carbon ethylene bridge, a structural arrangement that enables it to form exceptionally stable five-membered chelate rings with transition metals. This chelating geometry works particularly well with palladium, platinum, nickel, rhodium, and ruthenium — metals that sit at the heart of modern homogeneous catalysis. Because dppe binds through two phosphorus donor atoms simultaneously, it locks the metal center in place far more effectively than a monodentate phosphine ever could, resulting in catalyst systems that are more thermally stable, more selective, and more reliably reproducible across production batches.

What makes dppe genuinely compelling from a commercial standpoint is the breadth of reactions it enables. From Suzuki-Miyaura and Heck cross-couplings in pharmaceutical synthesis, to hydrogenation and carbonylation reactions in fine chemical manufacturing, dppe-based metal complexes have proven themselves across an extraordinary range of transformations. The compound is not merely a laboratory curiosity; it is a workhorse reagent that underpins large portions of the global specialty chemical and active pharmaceutical ingredient supply chain. Key suppliers operating in this space include Sigma-Aldrich (Merck KGaA), TCI Chemicals, Strem Chemicals, and Alfa Aesar (Thermo Fisher Scientific), all of which maintain extensive phosphine ligand portfolios serving both research-scale and bulk industrial requirements.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308098/bisethane-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities that are beginning to attract serious commercial investment.

Powerful Market Drivers Propelling Expansion

- Expanding Role of Homogeneous Catalysis in Pharmaceutical and Fine Chemical Synthesis: The single most powerful driver of dppe demand is the relentless growth of transition-metal-catalyzed synthesis in pharmaceutical manufacturing. Palladium-catalyzed cross-coupling reactions — Suzuki, Heck, Negishi, and Buchwald-Hartwig amination among them — have become foundational tools in the synthesis of active pharmaceutical ingredients, and dppe is one of the most widely employed ligands in these reaction classes. As global pharmaceutical R&D expenditure continues to rise, particularly in oncology and small-molecule drug development, the demand for reliable, high-purity ligands such as dppe grows correspondingly. The pharmaceutical industry's emphasis on process efficiency and yield optimization further reinforces the case for well-characterized bidentate phosphine ligands, because controlling the steric and electronic environment around the metal center directly translates into improved selectivity and reduced downstream purification costs.

- Growth in Organometallic Chemistry Research and Academic Procurement: The sustained global surge in organometallic chemistry and catalysis research has created a deep, durable base of academic demand for dppe. University research groups, government-funded laboratories, and private research institutions across North America, Europe, and Asia-Pacific routinely procure dppe for mechanistic studies, new catalyst development, and materials science investigations. The compound's versatility across multiple metal centers — including its widespread use in rhodium-catalyzed hydroformylation and palladium-mediated C-N bond-forming reactions — has secured its status as a standard reference ligand in inorganic chemistry curricula and graduate research programs worldwide. Furthermore, the increasing number of postgraduate programs in catalysis science, particularly across Asia-Pacific institutions, continues to expand the academic consumer base year after year. Dppe-ligated palladium complexes such as [Pd(dppe)Cl₂] rank among the most frequently cited catalyst precursors in cross-coupling literature, with thousands of peer-reviewed applications documented across synthetic organic chemistry journals.

- Green Chemistry and Process Efficiency Imperatives Driving Industrial Adoption: Beyond the pharmaceutical sector, the fine chemicals and agrochemical industries have increasingly adopted dppe-based catalytic systems for scalable synthetic routes where ligand-controlled selectivity reduces the need for costly separation and purification steps. Regulatory and market incentives to reduce stoichiometric reagent use, minimize heavy metal waste streams, and improve process mass intensity in manufacturing all favor the adoption of highly efficient, well-defined catalytic systems — and dppe fits squarely into this requirement. Process chemists value dppe because it delivers precise control over metal reactivity while offering broad substrate compatibility. This economic rationale, combined with tightening environmental compliance expectations across major manufacturing jurisdictions, reinforces the commercial case for dppe adoption in industrial settings and supports the market's steady forward momentum through the forecast period.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308098/bisethane-market

Significant Market Restraints Challenging Adoption

Despite its well-established value proposition, the dppe market faces meaningful structural challenges that temper its growth trajectory and require careful navigation by suppliers and end users alike.

- Sensitivity to Oxidation and Stringent Handling Requirements: One of the most practical challenges associated with dppe is its susceptibility to oxidative degradation upon exposure to ambient air. Like most tertiary phosphines, dppe can undergo surface oxidation, converting the catalytically active phosphine moieties to their corresponding phosphine oxides — a transformation that renders the compound catalytically useless. This sensitivity demands storage under inert atmosphere conditions, typically nitrogen or argon, along with Schlenk-line handling techniques and specialized moisture-resistant packaging. These requirements add logistical complexity and cost at every point in the supply chain. For smaller research groups in emerging markets where inert atmosphere infrastructure is less accessible, consistent use of dppe can become genuinely challenging, and this constrains market penetration in certain geographies even where underlying demand exists.

- Regulatory Pressures on Organophosphorus Compound Manufacturing and Transport: The production and international shipment of organophosphorus compounds, including the precursors required to synthesize dppe, are subject to increasingly stringent regulatory frameworks. Chlorodiphenylphosphine, a key synthetic intermediate, is classified as toxic and corrosive under multiple international transport regulations, and its procurement is subject to end-use declaration requirements in certain jurisdictions. While dppe itself does not carry the same level of restriction, manufacturers must maintain detailed compliance documentation throughout the supply chain. Cross-border trade in specialty organophosphorus chemicals is further complicated by evolving regulations in the European Union under REACH, in the United States under TSCA, and in China under MEE chemical registration requirements — all of which require substantial compliance investment and can delay market entry for new suppliers or novel product grades.

Critical Market Challenges Requiring Innovation

The inherently niche character of the dppe market presents structural challenges that go beyond simple supply and demand dynamics. Unlike commodity chemicals produced in thousands of metric tons annually, dppe is a specialty fine chemical supplied in gram-to-kilogram quantities for most applications and only occasionally in multi-kilogram volumes for industrial process chemistry. This low-volume market structure limits manufacturers' ability to achieve economies of scale, sustaining relatively high per-unit costs that can discourage procurement by cost-sensitive buyers. The market is further fragmented by purity grade — with ultra-high-purity research grades commanding significant premiums over technical-grade material — which complicates inventory planning and supply chain management for distributors serving a geographically dispersed customer base.

Additionally, competition from an expanding library of alternative bidentate phosphine ligands poses an ongoing challenge to dppe's market position. Ligands such as dppp (1,3-bis(diphenylphosphino)propane), dppb (1,4-bis(diphenylphosphino)butane), BINAP, and Xantphos each offer distinct bite-angle geometries and electronic profiles suited to particular catalytic applications. Process chemists routinely screen multiple ligand candidates during catalyst optimization, and dppe must continuously demonstrate performance advantages relative to these alternatives. The rise of high-throughput experimentation platforms in pharmaceutical process chemistry has made such comparative ligand screening faster and more systematic, which while beneficial for discovery, also means dppe faces ongoing competitive evaluation in every new drug development program.

Vast Market Opportunities on the Horizon

- Rising Adoption in Next-Generation Catalytic Applications Including Electrochemistry and Materials Science: Beyond its established role in homogeneous catalysis, dppe is finding growing application in emerging fields that represent meaningful long-term demand diversification. In coordination chemistry and materials science, dppe-bridged metal complexes are being investigated as components of luminescent materials, molecular wires, and single-molecule magnets — areas of active research with potential commercial pathways in organic electronics and sensing technologies. In electrochemistry, dppe-ligated nickel and cobalt complexes have been studied as electrocatalysts for hydrogen evolution and CO₂ reduction reactions, positioning the ligand within the rapidly expanding domain of sustainable energy research. These emerging application areas, while currently at early to mid-stage research phases, represent real and growing demand diversification opportunities for suppliers who engage proactively with academic and industrial programs in these adjacent fields.

- Expansion of Pharmaceutical Contract Manufacturing and Custom Synthesis in Asia-Pacific: The Asia-Pacific region, particularly China and India, has emerged as a major global hub for pharmaceutical contract manufacturing organizations and contract research organizations that routinely employ transition-metal-catalyzed cross-coupling chemistry in API and intermediate synthesis. As these organizations scale their capabilities and pursue regulatory approval for increasingly complex small-molecule drug substances, their demand for high-quality, well-characterized ligands such as dppe is expected to grow substantially. Several Chinese specialty chemical manufacturers have already invested in organophosphorus synthesis capabilities, creating both a localized supply base and a rapidly growing domestic consumer market. This dual dynamic — supply development alongside demand expansion — suggests Asia-Pacific will account for an increasing share of global dppe market activity over the coming decade, offering suppliers with established quality credentials and regulatory documentation significant commercial opportunities in this geography.

- Premiumization Toward High-Purity and Application-Specific Ligand Formulations: There is a clear and accelerating trend toward premium-grade dppe products in the market, driven by pharmaceutical manufacturers and precision catalyst developers who require GMP-compliant materials with documented lot-to-lot consistency and full analytical characterization. Ultra-high-purity grades exceeding 99% purity by ″¹P NMR command significant price premiums over standard commercial grades, and the share of market value attributable to these high-specification products is rising faster than overall volume growth. Suppliers with the analytical infrastructure and quality management systems to consistently deliver premium-grade dppe are well-positioned to capture disproportionate value growth as the pharmaceutical sector continues to scale its use of organometallic catalysis in manufacturing workflows.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into High-Purity Grade (≥98%), Ultra-High-Purity Grade (≥99%), and Technical Grade. Ultra-High-Purity Grade commands the most significant demand within the dppe market, driven by its critical role in precision catalytic applications where trace impurities can severely compromise reaction selectivity and yield. Research institutions and pharmaceutical manufacturers consistently prioritize this grade to ensure reproducibility in sensitive organometallic synthesis. High-Purity Grade remains broadly adopted across industrial-scale catalytic processes where cost-efficiency is balanced with acceptable performance standards. Technical Grade, while occupying a more limited niche, continues to serve exploratory laboratory work and preliminary feasibility studies where absolute purity thresholds are less stringent.

By Application:

Application segments include Homogeneous Catalysis, Pharmaceutical Synthesis, Agrochemical Synthesis, Academic & Research, and Others. The Homogeneous Catalysis segment currently dominates, owing to dppe's exceptional ability to stabilize a wide range of transition metal complexes and facilitate carbon-carbon and carbon-heteroatom bond-forming reactions at scale. However, Pharmaceutical Synthesis is the fastest-growing application area, reflecting the ongoing expansion of palladium-catalyzed cross-coupling chemistry in drug manufacturing pipelines. Agrochemical Synthesis leverages similar catalytic efficiencies for the production of crop protection compounds, while Academic & Research applications sustain foundational demand driven by continuous exploration of novel ligand-metal chemistry across institutions globally.

By End-User Industry:

The end-user landscape includes Pharmaceutical & Biotechnology Companies, Chemical Manufacturers, Academic & Research Institutions, and Agrochemical Companies. Pharmaceutical & Biotechnology Companies constitute the leading end-user segment, underpinned by the intensifying demand for high-efficiency organometallic catalysts in drug discovery and API manufacturing. These organizations require dppe with stringent quality specifications to meet regulatory compliance and ensure batch-to-batch consistency. Chemical Manufacturers form a substantial secondary consumer base, utilizing dppe-based systems in fine and specialty chemical synthesis at both pilot and commercial scales. Academic & Research Institutions drive innovation through fundamental studies, while Agrochemical Companies round out the landscape by employing dppe-facilitated catalysis in the efficient production of herbicides, fungicides, and insecticides.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308098/bisethane-market

Competitive Landscape:

The global 1,2-Bis(diphenylphosphino)ethane market is characterized by a concentrated base of specialty fine chemical and organophosphorus compound manufacturers, with competition driven primarily by product purity, supply reliability, technical support capabilities, and pricing at volume. The market is dominated by established fine chemical suppliers with deep expertise in air-sensitive organophosphorus chemistry and stringent quality control capabilities. MilliporeSigma (Sigma-Aldrich / Merck KGaA), Thermo Fisher Scientific (Alfa Aesar), and TCI Chemicals collectively command a substantial share of global supply, underpinned by their broad reagent portfolios, extensive global distribution networks, and well-established reputations for consistent high-purity product offerings. Strem Chemicals, a recognized specialist in inorganic and organometallic compounds, maintains a significant position supplying high-purity dppe to research and catalysis customers. Beyond the established multinationals, a growing number of specialty fine chemical manufacturers in China — including Shandong Dongchang Fine Chemical Technology and Warshel Chemical — have invested in organophosphorus ligand production capabilities, introducing cost-competitive supply options that are reshaping procurement dynamics, particularly for buyers in Asia-Pacific markets. The competitive strategy across the industry is heavily focused on continuous quality improvement, expansion of analytical certification offerings, and the development of long-term supply relationships with pharmaceutical customers whose procurement processes demand rigorous vendor qualification.

List of Key 1,2-Bis(diphenylphosphino)ethane (CAS 1663-45-2) Companies Profiled:

● MilliporeSigma (Sigma-Aldrich / Merck KGaA) (Germany / USA)

● Thermo Fisher Scientific (Alfa Aesar) (USA)

● TCI Chemicals (Japan)

● Strem Chemicals (USA)

● ABCR GmbH (Germany)

● Fluorochem Ltd (United Kingdom)

● Shandong Dongchang Fine Chemical Technology Co., Ltd. (China)

● Oakwood Chemical (USA)

● Warshel Chemical Ltd. (China)

The competitive strategy across the dppe market is overwhelmingly focused on delivering verified purity, comprehensive analytical documentation, and reliable supply continuity — alongside forming strategic partnerships with pharmaceutical and fine chemical end-users to co-develop application-specific catalyst systems, thereby securing durable long-term demand.

Regional Analysis: A Global Footprint with Distinct Leaders

● Asia-Pacific: Stands as the leading region in the global dppe market, driven by the region's commanding position in fine chemical manufacturing, pharmaceutical API synthesis, and homogeneous catalysis research. China, in particular, hosts a substantial and growing base of specialty chemical manufacturers and API producers, while Japan's advanced materials research institutions and South Korea's expanding pharmaceutical sector further reinforce regional demand. India's rapidly growing generic pharmaceutical industry is an increasingly important consumer as API manufacturers adopt metal-catalyzed synthesis routes to improve process efficiency. The presence of well-developed chemical supply chains and cost-competitive manufacturing infrastructure collectively positions Asia-Pacific as the dominant force shaping global dppe consumption trends through 2034.

● North America: Represents a significant and mature market for dppe, underpinned by the region's world-leading pharmaceutical industry, thriving academic catalyst development community, and strong base of contract research organizations that routinely employ palladium-dppe complexes in drug discovery and process chemistry workflows. The U.S. market is characterized by strong emphasis on product quality, regulatory compliance, and supply traceability, as dppe used in pharmaceutical synthesis must meet stringent purity and documentation requirements. While North America does not match Asia-Pacific in production volume, it remains a critical market defined by high-value applications and premium-grade product requirements.

● Europe: Holds a well-established position in the global dppe market, supported by the region's historically strong chemical industry, world-class pharmaceutical manufacturers, and prominent academic research institutions in Germany, Switzerland, the United Kingdom, France, and the Netherlands. European regulatory frameworks emphasizing chemical safety and environmental compliance influence procurement practices, with buyers prioritizing certified, high-purity suppliers. The region's well-organized specialty chemical distribution networks ensure reliable supply access for both research and industrial end users, maintaining Europe as a consistently important segment in the global market landscape.

● South America and Middle East & Africa: These regions currently represent smaller but gradually developing segments of the global dppe market. South America's demand is primarily concentrated in Brazil, driven by its growing pharmaceutical manufacturing base and expanding academic chemical research sector. The Middle East and Africa remain at early stages, with demand largely limited to research institutions and select pharmaceutical operations. However, ongoing investments in chemical industry diversification across Gulf Cooperation Council countries, combined with the maturation of pharmaceutical and fine chemical industries in Brazil and South Africa, suggest these regions will contribute increasing shares of global dppe consumption over the longer term, even if they remain secondary markets through the near to medium term.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308098/bisethane-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308098/bisethane-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/