800G Digital Coherent Optics (DCO) Transceiver Market, Trends, Business Strategies 2026-2034

The global 800G Digital Coherent Optics (DCO) Transceiver Market, valued at a robust US$ 899 million in 2025, is on a trajectory of significant expansion, projected to reach US$ 1,634 million by 2032. This growth, representing a compound annual growth rate (CAGR) of 9.1%, is detailed in a comprehensive new report published by Semiconductor Insight. The study highlights the pivotal role of high‑capacity coherent optics in enabling the next generation of data center interconnects, long‑haul carrier networks, and emerging AI‑driven workloads.

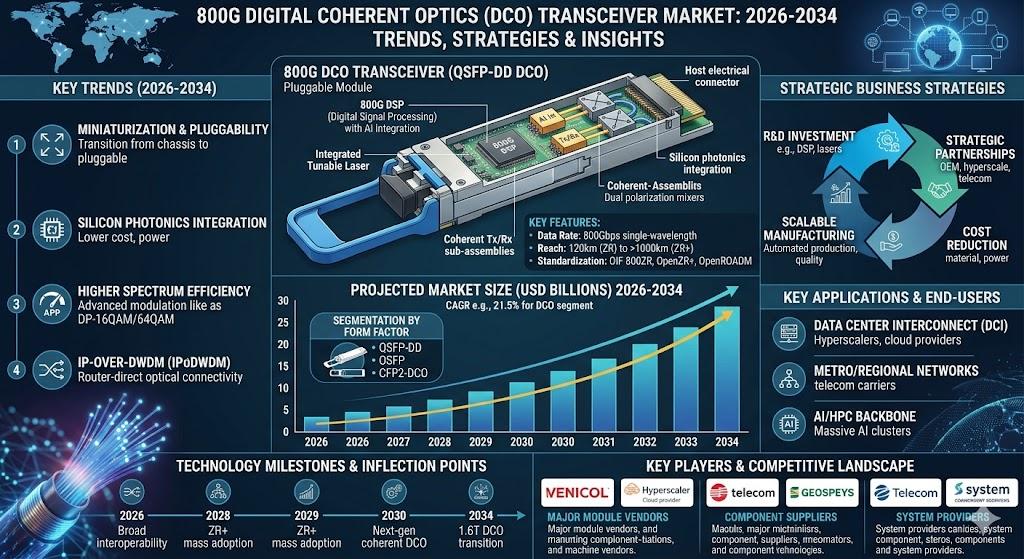

800G DCO transceivers combine advanced digital signal processing (DSP), coherent detection, and industry‑standard form factors such as QSFP‑DD and OSFP to deliver unprecedented bandwidth density while maintaining power efficiency and low latency. Their ability to support reach distances up to 120 km for data‑center interconnect (DCI) and beyond 500 km for metro/regional deployments makes them indispensable for operators seeking to upgrade legacy 400G infrastructure without extensive fiber rebuilds. By integrating high‑order modulation formats and forward error correction, these modules future‑proof networks against the anticipated 1.6 Tbit/s evolution.

Download FREE Sample Report:

800G Digital Coherent Optics (DCO) Transceiver Market - View in Detailed Research Report

The surge in demand is fueled primarily by hyperscale cloud providers that are scaling out distributed computing resources across continents. As artificial intelligence, machine learning, and real‑time analytics workloads consume ever‑greater data volumes, the need for terabit‑class links becomes a strategic imperative. Telecom service providers, in parallel, are refreshing their backbone and metro networks to support 5G backhaul, edge‑to‑cloud services, and the growing volume of video traffic. The convergence of these forces is reshaping network architectures, encouraging a shift from traditional intensity‑modulation/direct‑detection (IM/DD) solutions toward coherent optics that can sustain higher spectral efficiency and longer reaches without costly repeaters.

Data Center & Telecom Expansion: The Primary Growth Engine

The report identifies the exponential expansion of hyperscale data center ecosystems as the paramount driver for 800G DCO transceiver adoption. Cloud giants are investing heavily in inter‑data‑center links that exceed 100 Gbps per wavelength, reducing the number of fibers required while simplifying network management. In parallel, telecom operators are modernizing legacy DWDM platforms to integrate coherent modules, enabling seamless migration pathways from 400G to 800G without wholesale infrastructure turnover. The combined effect of these investments is projected to generate a sustained uplift in module shipments, reinforcing the market’s upward momentum.

“The concentration of data center footprints in North America and the rapid rollout of carrier‑grade DWDM networks across the Asia‑Pacific region, which together account for more than 70 % of projected 800G transceiver volume, is a key factor in the market’s dynamism,” the report states. With global capital expenditures in data‑center and telecom infrastructure exceeding US$ 300 billion through 2030, the appetite for coherent optics that can deliver both reach and capacity is set to intensify.

Get Full Report Here:

800G Digital Coherent Optics (DCO) Transceiver Market, Trends, Business Strategies 2026-2034 - View in Detailed Research Report

COMPETITIVE LANDSCAPE

Key Industry Players

Top Leaders Driving 800G DCO Transceiver Market Innovation

The 800G Digital Coherent Optics (DCO) Transceiver market exhibits a concentrated competitive structure dominated by a handful of technology leaders, including II‑VI Incorporated (now Coherent Corp.), Lumentum, and Zhongji Innolight. These top players collectively command a significant revenue share, with the global top five manufacturers accounting for approximately 70‑80 % of the market in 2025 based on industry surveys. The market’s oligopolistic nature stems from the high barriers to entry posed by advanced Digital Signal Processing (DSP), coherent detection integration, and compliance with QSFP‑DD and OSFP specifications. Leaders like Coherent and Lumentum excel in providing high‑capacity solutions for Data Center Interconnect (DCI) up to 120 km and metro/regional networks exceeding 500 km, fueling growth projected from US$ 899 million in 2025 to US$ 1,634 million by 2032 at a 9.1 % CAGR.

Beyond the frontrunners, niche and regional significant players such as Hisense Broadband, Accelink Technologies, and Eoptolink are carving out substantial positions, particularly in Asia‑Pacific where cost‑effective manufacturing drives adoption in metropolitan area networks and other applications. Semiconductor giants like Cisco, Broadcom, and Intel contribute through integrated optics and pluggable modules, enhancing ecosystem compatibility. Emerging challengers including HG Genuine Optoelectronics and others focus on specialized DWDM capabilities, intensifying competition via innovations in power efficiency and reach. This dynamic fosters ongoing mergers, R&D investments, and supply‑chain optimizations amid rising demand for low‑latency, high‑speed data transmission.

List of Key 800G Digital Coherent Optics (DCO) Transceiver Companies Profiled

-

II-VI Incorporated (Coherent Corp.)

-

Zhongji Innolight

-

Accelink Technologies

-

Intel

-

HG Genuine Optoelectronics (Hgtech)

-

Source Photonics

-

Infinera

-

Ciena

-

Nokia

-

Fiberhome Telecommunication

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

QSFP-DD Specification

|

| By Application |

|

Data Center Interconnection (DCI)

|

| By End User |

|

Hyperscale Cloud Providers

|

| By Reach Distance |

|

Up to 120km (DCI)

|

| By Network Type |

|

Dense Wavelength Division Multiplexing (DWDM)

|

Regional Analysis: 800G Digital Coherent Optics (DCO) Transceiver Market

Hyperscalers in North America drive 800G DCO transceiver uptake for backbone interconnects, prioritizing low‑latency and high‑density solutions to handle explosive data growth from cloud services and edge computing.

Silicon Valley and other tech hubs spearhead R&D in coherent optics, focusing on advanced modulation formats and pluggable modules that enhance spectral efficiency for 800G Digital Coherent Optics (DCO) Transceiver Market applications.

Partnerships between transceiver vendors, DSP providers, and carriers streamline 800G interoperability testing, accelerating market readiness and ecosystem maturity.

Ongoing fiber optic expansions and 5G backhaul upgrades create fertile ground for 800G DCO transceivers, supported by private equity and public funding focused on digital transformation.

Europe

Europe exhibits steady progress in the 800G Digital Coherent Optics (DCO) Transceiver Market, bolstered by stringent data sovereignty regulations and pan‑continental fiber networks. Telecom incumbents invest in coherent upgrades for subsea cables and metro aggregations, emphasizing energy‑efficient designs amid green initiatives. Research consortia drive advancements in photonic integration, positioning the region for competitive edge in long‑haul deployments. Challenges include fragmented standards across member states, yet EU‑funded projects harmonize efforts. Hyperscale expansions by global players further stimulate demand, fostering a balanced growth trajectory.

Asia‑Pacific

Asia‑Pacific emerges as a high‑growth area in the 800G DCO Transceiver Market, fueled by massive data‑center builds in key economies and intra‑regional connectivity demands. Manufacturing prowess enables cost‑effective production scaling, while telcos upgrade DWDM systems for 800G capacities. Rapid urbanization and digital economy policies propel adoption in smart cities and enterprise networks. Supply‑chain localization reduces dependencies, though IP protection concerns persist. The region's volume‑driven approach complements North America's innovation leadership.

South America

South America shows nascent development in the 800G Digital Coherent Optics (DCO) Transceiver Market, with focus on bridging digital divides through undersea cable upgrades and terrestrial fiber expansions. Leading operators prioritize coherent tech for long‑distance links across diverse terrains. Economic stabilization attracts foreign investments in data infrastructure, yet regulatory hurdles and currency volatility temper pace. Emerging hyperscalers lay groundwork for future 800G needs, promising accelerated uptake.

Middle East & Africa

The Middle East & Africa region advances cautiously in the 800G DCO Transceiver Market, leveraging oil‑funded diversification into tech hubs and smart‑nation visions. Gulf states invest heavily in data sovereignty via local data centers requiring high‑capacity optics, while African telcos enhance backbones for mobile broadband. Geopolitical tensions challenge supply continuity, but strategic alliances with global vendors mitigate risks. Visionary projects position the area for leapfrog growth in coherent networking.

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high‑technology industries. Our in‑depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high‑quality, data‑driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us