High Bandwidth Memory (HBM3, HBM3E, HBM4) Market, Trends, Business Strategies 2026-2034

The global High Bandwidth Memory (HBM3, HBM3E, HBM4) Market is accelerating at an unprecedented pace, driven by the explosive demand for AI accelerators, high‑performance computing (HPC) clusters, and next‑generation graphics processing units (GPUs). With AI models growing in size and complexity, system designers are turning to HBM to deliver the extreme memory bandwidth and capacity required for training and inference workloads that cannot be satisfied by conventional DDR memory architectures.

High Bandwidth Memory is a vertically‑stacked DRAM technology that leverages through‑silicon‑via (TSV) interconnects to achieve gigabytes‑per‑second data rates while maintaining a compact footprint. By placing multiple memory dies on top of each other and linking them through an ultrawide bus, HBM delivers up to ten times the bandwidth of traditional DRAM, enabling faster data movement, lower power consumption per bit transferred, and reduced latency for compute‑intensive applications.

Download FREE Sample Report:

High Bandwidth Memory (HBM3, HBM3E, HBM4) Market - View in Detailed Research Report

Artificial Intelligence & HPC: The Primary Growth Engine

The report identifies the rapid expansion of AI and HPC workloads as the paramount driver for HBM adoption. AI hardware manufacturers and hyperscale cloud service providers are the dominant end‑users, accounting for the majority of memory demand as they build dedicated training clusters and inference farms. The convergence of generative AI, large language models, and real‑time inference services is creating a structural need for memory solutions that can sustain multi‑terabyte data streams without bottlenecks.

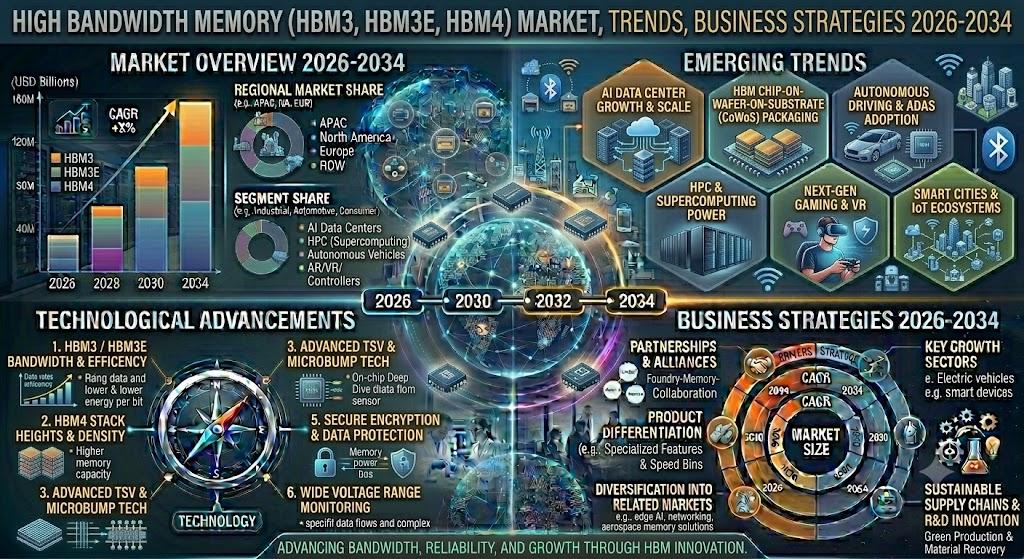

“The concentration of AI‑focused data centers in the Asia‑Pacific region, which consumes an estimated 75% of global HBM volumes, is a key factor in the market’s dynamism,” the study notes. Global investment in AI‑centric semiconductor fabs and advanced packaging facilities is projected to exceed $200 billion through 2034, reinforcing the strategic importance of HBM in the compute stack.

Read Full Report: https://semiconductorinsight.com/report/heating-jackets-market/

Market Segmentation: HBM Types and Application Landscape

The report provides a detailed segmentation analysis, offering a clear view of the market structure and key growth segments:

Segment Analysis:

By Type

- HBM3

- HBM3E

- HBM4

By Application

- Artificial Intelligence & Machine Learning Accelerators

- High‑Performance Computing (HPC)

- Graphics Processing Units (GPUs)

- Network Switching & Routing

- Others

By End User

- Hyperscale Cloud Service Providers

- AI Hardware Manufacturers & Semiconductor Companies

- Research & Academic Institutions / HPC Centers

- Telecommunications & Networking Companies

Segment Analysis Table

| Segment Category | Sub‑Segments | Key Insights |

| By Type |

|

HBM3E currently dominates, driven by rapid adoption in cutting‑edge AI accelerators and high‑performance GPU architectures.

|

| By Application |

|

Artificial Intelligence & Machine Learning Accelerators dominate the application landscape, reshaping memory architecture requirements globally.

|

| By End User |

|

Hyperscale Cloud Service Providers are the dominant end‑user segment, anchoring the commercial trajectory of HBM3, HBM3E, and HBM4.

|

| By Technology Architecture |

|

2.5D Integration via Silicon Interposer currently leads as the most widely adopted packaging architecture for HBM.

|

| By Supply Chain Tier |

|

Tier 1 HBM DRAM Manufacturers hold decisive control over production volume and technology timelines.

|

Competitive Landscape

COMPETITIVE LANDSCAPE

Key Industry Players

High Bandwidth Memory (HBM3, HBM3E, HBM4) Market: Competitive Dynamics and Strategic Positioning of Leading Semiconductor Players

The global High Bandwidth Memory (HBM3, HBM3E, HBM4) market is dominated by a concentrated group of advanced semiconductor manufacturers, with SK Hynix holding a leading position as the foremost supplier of HBM solutions worldwide. SK Hynix was the first to achieve mass production of HBM3E in early 2024 and secured a landmark supply agreement with NVIDIA for integration into its H200 and Blackwell GPU architectures, cementing its technological edge in the AI accelerator space. The company's deep investment in through‑silicon‑via (TSV) stacking technology and its strategic roadmap toward HBM4 development further reinforce its competitive moat. Samsung Electronics and Micron Technology represent the other two pillars of the HBM triopoly, both aggressively scaling HBM3E output while concurrently advancing next‑generation HBM4 architectures to address surging demand from hyperscale cloud providers, AI hardware manufacturers, and high‑performance computing (HPC) cluster operators globally.

Beyond the primary memory manufacturers, the HBM ecosystem encompasses a broader network of critical enablers including advanced packaging specialists, substrate suppliers, and chipmakers whose products integrate HBM solutions directly into end platforms. Companies such as NVIDIA and AMD are pivotal demand drivers, designing flagship GPU and AI accelerator products - including the H100, H200, Instinct MI300X, and Blackwell series - that rely exclusively on HBM3 and HBM3E for their extreme memory bandwidth requirements. TSMC and ASE Technology play essential roles in advanced packaging and chip‑on‑wafer‑on‑substrate (CoWoS) integration processes that physically bond HBM stacks to logic dies. Additionally, Cadence Design Systems and Synopsys provide critical EDA tooling and IP that underpin HBM interface design and verification, while companies like Rambus contribute standardization and memory interface controller IP critical to HBM adoption across next‑generation platforms.

List of Key High Bandwidth Memory (HBM3, HBM3E, HBM4) Companies Profiled

-

Advanced Micro Devices, Inc. (AMD)

-

Taiwan Semiconductor Manufacturing Company (TSMC)

-

ASE Technology Holding Co., Ltd.

-

Rambus Inc.

-

Cadence Design Systems, Inc.

-

Synopsys, Inc.

-

Intel Corporation

-

Amkor Technology, Inc.

-

JEDEC Solid State Technology Association

-

Graphcore Limited

-

Cerebras Systems

These companies are focusing on technological advancements such as tighter TSV pitch, hybrid bonding, and co‑design of memory‑logic interfaces, while also pursuing geographic expansion into high‑growth regions like Asia‑Pacific to capitalize on emerging AI‑driven opportunities.

Emerging Opportunities in Data Center, Edge AI, and Automotive Segments

Beyond the core AI‑training market, the report highlights several fast‑growing verticals that are beginning to shape HBM demand. Edge AI devices, which require high bandwidth in a power‑constrained form factor, are exploring low‑profile HBM3E footprints to enable on‑device inference for autonomous vehicles and industrial robots. The automotive sector, especially advanced driver‑assistance systems (ADAS) and next‑generation infotainment platforms, is evaluating HBM‑enabled compute modules to meet stringent latency and safety requirements. Meanwhile, hyperscale data centers continue to expand AI‑focused clusters, with multi‑tenant AI platforms leveraging HBM4 to support next‑generation foundation models that will dominate the AI landscape beyond 2030.

Report Scope and Availability

The market research report offers a comprehensive analysis of the global and regional High Bandwidth Memory markets from 2026 – 2034. It provides detailed segmentation, market size forecasts, competitive intelligence, technology trends, and an evaluation of key market dynamics, including supply‑chain constraints, pricing pressures, and strategic collaborations.

Get Full Report Here:

High Bandwidth Memory (HBM3, HBM3E, HBM4) Market, Trends, Business Strategies 2026-2034 - View in Detailed Research Report

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high‑technology industries. Our in‑depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high‑quality, data‑driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us